How Old is the Oldest Person You Know?

The Prudential commercial that aired during Super Bowl 47 features what Steven Strogatz calls the most viewed histogram of all time.

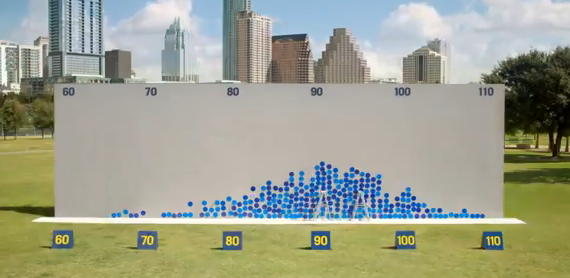

According to the commercial people were asked the age of the oldest person they know, and their answers were plotted. The resulting histogram is somewhat “normal” looking, and the average age is in the low 90s.

The commercial’s message is clear: “Look at how old people get! You need to be better prepared for your retirement! Come see a Prudential representative today.”

This is a good example of the subtle ways mathematics can be used to manipulate the opinions of the quantitatively unsophisticated.

The above histogram is intentionally designed to mislead viewers into thinking they may be significantly unprepared for retirement. The average life expectancy in the US is around 78 years, but this number may not be shocking enough for advertisitng purposes. So instead of life expectancy, Prudential used age of the oldest person you know, a data set whose average is about 15 years higher.

Showing a histogram that suggests people are likely to live into their 90s might motivate some viewers to head down to their local Prudential office, worried that they aren’t properly prepared for retirement. But the data on display here isn’t really relevant, and the difference is so subtle that most people won’t notice the distinction. In reality, the age of the oldest person you know has very little to do with how long you will live.

Imagine asking each member of a large group to name the salary of the highest-paid person they know. The average of these responses, the average highest-known-salary, will almost certainly be much higher than the average salary of the people in the group. It would be ridiculous to try to estimate the average salary of the group by looking at the average highest-known-salary, but in a sense, that is exactly what Prudential is doing in this commercial.

The fact that they are doing it intentionally to further their interests provides yet another example of the vital need for quantitative literacy in today’s world.

21 Comments

Mike Lawler · May 28, 2013 at 10:39 am

I don’t see this one quite the same way.

First, though, I agree completely that understanding the financing your retirement is one of the best examples of the vital need for quantitative literacy. Absolutely. Everyone should understand concepts such as compound interest, discount rates, and present value. Sadly, few people do – much to their own detriment, I’m afraid.

Second, and more to the point of your article, for me the example you use in your last paragraph is not the right one. The distribution of salary and age in a population are not similar at all. For example, I am 41 years old. There is no one in the world who is 4x my age, but I don’t have to look outside of the office I work in to find people who make 4x my salary. The distinction between these two types of distributions was described well by Nassim Taleb in his books “Fooled by Randomness” and “Black Swan.” He used the descriptive terms “mediocristan” and “extremistan.”

In mediocristan, roughly speaking, any measurement of a large group is going to have statistics that don’t vary that much. His example was height, but age also works. If you have 999 people in a room and then add the oldest person in the world to the room, the average age shifts up, but not by that much.

In extremistan, again roughly speaking, the statistics can vary dramatically even for large groups. His example was net work, but salary also works well. If you have 999 people in a room and then add the person with the highest salary in the world from the previous year, the average salary of the new group looks nothing at all like the prior average. In fact, the average salary of the new group will be approximately the salary of the last person divided by 1,000.

Following Taleb’s language, it is difficult to extend a conclusion from extremistan to mediocristan (and the other way around). I think that comparing statistics about salary and age is difficult.

MrHonner · May 28, 2013 at 8:23 pm

Mike-

The real issue here is the intentional substitution of a familiar piece of data (average life span) with an unrelated one (average oldest person known) for the purposes of advancing a particular agenda.

The salary metaphor is peripheral. I understand what you’re saying about how the ranges of the various data sets makes comparison trickier, but what I’m comparing is how, in both cases, the values “average X” and “average highest known X” are not related. In the case of age, the two numbers may be closer because the data ranges are tighter, but that doesn’t mean they are any more related.

Mike Lawler · May 29, 2013 at 7:41 am

I find the question you are posing here to be pretty interesting.

According to the Social Security Administration, a 65 year old should expect to live to about 84 (splitting the male/female difference) and one in four will live to age 90. See the link here:

http://www.ssa.gov/planners/lifeexpectancy.htm

So, if you are 65 and planning for retirement, if you have enough money set aside to life to age 90, you only have a 1 in 4 chance of running out of money. If you want to improve your odds to 1 in 10, you’ll need to set aside about 5 more years worth of money.

So, if you are planning for retirement, how much money should you save? Is a 1 in 4 chance of running out of money a good bet, or do you want to be more conservative. I’d guess the answer will vary quite a bit from person to person. Of course, this is theory not practice since hardly anyone has that amount of money saved by age 65.

Glancing at the Prudential graph, it looks like the median age of the oldest person someone knows is about 90.

I agree that looking at the age the oldest person you know is likely to give an overestimate of your expected age at death. However, it isn’t as clear to me that looking at the age of this person and then planning on setting aside enough money to life to that age is necessarily a bad strategy.

Doris Tomlin · May 29, 2013 at 11:52 pm

MrHonner, I think you are off-base in your criticism of Prudential’s commercial message. I agree with Mike Lawler in both of his comments.

When planning for retirement, if you are going to finance your entire retirement yourself, you must consider the possibility — actually the RISK — that you will outlive your money. Planning to save enough to live to ones AVERAGE life expectancy will, on average, fail half the time, by definition! Prudential’s commercial is properly calling attention to the longevity risk that a worker faces when planning for retirement financing.

True, many Americans who are heeding the intended message of Prudential’s commercial are over-saving for retirement, but none of us will know for many years which individuals have over-saved and which individuals have still not saved enough.

I believe that share-the-risk retirement plans such as Social Security, defined-benefit pension plans, and annuities are the more reasonable way to approach retirement funding for the majority of people. If you drop dead without ever drawing your pension or your Social Security, the money you contributed or deferred is not benefiting you directly, but at that point, you have no need of it! If you by chance do live to be as old as the oldest person you know, or the oldest person that anyone knows, you will still have retirement income at that superannuated age because of those who did not reach their average life expectancy. In either case, the cost to you will be the cost to finance a retirement until your average life expectancy.

MrHonner · May 30, 2013 at 6:41 am

It’s a fair point that “average life expectancy” may not be the right target in retirement planning, as many people will live past that age (although probably not half–I don’t think it’s the median life expectancy).

And yes, over-saving may be the prudent strategy. But this by itself doesn’t validate using the oldest person you know, or the average oldest known person, as the target age. One could argue that, in order to be really safe, you should expect to live as long as the oldest person who has ever lived. I’m not sure this strategy is substantially less valid than the the oldest-person-you-know strategy.

Mike Lawler · May 30, 2013 at 7:22 am

My point isn’t that I think the criticism of Prudential is unfair – after all, if the main point of the original post was simply that they were just bending the facts a little in their advertising, I doubt many folks would find that point to be particularly interesting or surprising.

Rather, what I’m surprised at here is that they way they are spinning their story here seems to me to lead to a strategy for saving for retirement that doesn’t seem to be all that crazy. At least at first glance.

In a way it reminds me of the Marriage Problem. I guess Wikipedia is a good, quick link (though I first learned of this puzzle in Steven Krantz’s wonderful book “Techniques of Problem Solving”):

http://en.wikipedia.org/wiki/Secretary_problem

This problem seems unsolvable at first, but there is an optimal technique that turns out to be quite surprising, at least to me.

In any case, I thought it was quite fun and interesting to think through the ideas of retirement saving and how it may relate to the oldest person you know.

As a completely unrelated aside, if you’ve not seen Krantz’s book, it is a fun read. Through a strange accident, I have two copies that just sit on my shelf gathering dust and would be happy to send you one. He (or the AMS) has probably updated the book since 1996, but this version is still ok, I think! In addition to the Marriage Problem which he discusses, Bertrand’s Paradox is one of the most interesting geometry puzzles I’ve ever run across. If you’d like this spare copy of the book, feel free to shoot me a good address at mjlawler at yahoo dot com.

Cut the Knot has a good discussion of Bertrand’s Paradox, btw:

http://www.cut-the-knot.org/bertrand.shtml

Brian · June 5, 2013 at 6:55 pm

Mike,

I think you miss the point of the last graph completely. I don’t think that the author was trying to show similarity in the distributions of ages and salaries. i think he was trying to point out that deriving the average age by asking about the oldest person you know would give bad result. Similarly, a bad result about income would also be created by asking about highest salaries.

This is an article about the intentional picking of a skewed method\dataset rather than any real correlations between ages and incomes.

Mike Lawler · June 5, 2013 at 8:54 pm

Well, let me try to explain my point more clearly.

First, though I want to be extra careful and leave no doubt whatsoever that I found Mr. Honner’s post here to be extremely interesting and that I have really enjoyed spending time thinking about it in the last week. This is a fascinating topic and one where I’m not sure the answer is at all obvious.

The point of the Prudential ad (besides trying to get folks to hand over money to them, of course) is to get people thinking about retirement and how long they might live. To think through that topic properly you need to think about your expected age at death. You probably also need to think through how much financial cushion you want to have in the event you live past that expected age.

In the paragraph you reference, I do agree completely with the statement – “It would be ridiculous to try to estimate the average salary of the group by looking at the average highest-known-salary . . . .” I believe it would be ridiculous because salaries tend to follow power law distributions and for these types of distributions taking the average of things that are in the tail of the distribution will not yield an answer that is anywhere near the mean. (It wouldn’t be a surprise at all if when you and I wrote down the highest salary collected by anyone we know, that one of our numbers was more than double the other one, for example.)

I’m not, however, totally on board with the next statement in that paragraph – “. . . in a sense, that is exactly what Prudential is doing in this commercial.” First, the goal here is not to try to get the average age of the group. Rather, the goal is to estimate the average age at death for an individual in the group (and then maybe also to assess how much cushion a member of the group might need for living past that average). Ages do not come in power law distributions. There is no chance whatsoever that the oldest person you know is 2x as old the oldest person that I know, for example. So, if we are going to conclude that the Prudential commercial is misleading, at minimum we’d want to have an analogy that had roughly similar statistics.

Beyond the statistics, though, as I mentioned in a comment above, I’m not as convinced that the dots in the graph are as misleading as Mr. Honner thinks they are. Just glancing at the graph, it looks as though the median “highest age of a person you know” is around 90. In saving for retirement, setting aside enough money to live to age 90 doesn’t seem to me to be an obviously bad strategy. In fact, the page on the Social Security site I linked to indicates that about 25% of people who are 65 will live past 90, so setting aside enough money to live to age 90 might arguably be not conservative enough for many individual’s own tastes.

In a comment below, Mr. Honner indicates that the connection between the Prudential graph and a good age to save to in retirement is just coincidental. Again, I’m just not as convinced of that. In fact, the more I’ve thought about it over the last couple of days, the more I think that there is a striking relationship between the graph Prudential shows and the Marriage Problem I mentioned in a comment above. The optimal solution in that problem is roughly to sample about (1/e)th of the data set and then use the data you’ve collected so far to make a decision. With the Prudential graph, you’ve got a reasonably large data set listing the age of “the oldest person you know” and the median of that set seems to give a decent number for retirement planning purposes. It may very well be that the surprising math behind the solution of the Marriage Problem applies quite well to the problem of selecting an age to assume you will live to for purposes of retirement planning. If so, the fact that (i) the median of the Prudential graph is 90 and (ii) that age 90 is a reasonable age to assume you will live to for purposes of retirement planning is actually not a coincidence at all.

Evelyn Lamb · May 28, 2013 at 12:10 pm

At least it’s not those terrible Geico commercials! Why would a bodybuilder want to direct traffic? He’s standing in the middle of a hot, busy street with exhaust spewing all over him. Are we to believe that bodybuilders are so vain that the pleasure they get by posing for people outweighs the clear crappiness of the task?

It does make sense to be prepared for the long side of one’s possible lifespan, even if it’s unlikely you’ll outlive the oldest person you know. (Though for the record, that’s exactly what I intend to do.)

MrHonner · May 28, 2013 at 8:07 pm

I almost marked this comment as spam because the first thing I saw was “Why would a bodybuilder want to direct traffic?”, a very bot-like remark.

But cheers to you, Evelyn, and here’s hoping we all outlive the oldest person everyone knows!

Evelyn Lamb · May 29, 2013 at 11:25 am

Perhaps I am a bot!

David Price · May 28, 2013 at 2:38 pm

I agree that the average salary analogy is a bit iffy, it’s perhaps more like asking a child to name the tallest person they know and promising they will grow to that height.

I blogged about this a while back in connection with a billboard over the Midtown Tunnel (http://davidprice.wordpress.com/2013/03/29/the-first-person-to-live-to-150-is-alive-today/) because I was similarly struck by Prudential blatantly passing off outliers as measures of central tendency.

It’s also worth noticing that the Prudential sample in the TV ad is not random, it was taken near the hike and bike trail in my old neighborhood in Austin, Texas, one of the fitter and wealthier parts of the country!

MrHonner · May 28, 2013 at 8:29 pm

David-

As I replied to Mike, the salary metaphor is just to point out the absurdity in comparing “average X” and “average highest known X”. Although I do like your example of “Whose the tallest person you know?”.

To be honest, the first thing I thought of was bowling: Consider asking a group of bowlers “What the highest score you’ve ever heard of someone bowling?”, taking that average, and comparing that with their average score. But I figured not everyone was familiar with bowling.

And great catch on the “random” selection, although I’m not sure how much that would affect the results. After all, even poor and unhealthy people know someone really old, right?

Amy Hogan · May 28, 2013 at 10:52 pm

I too was irked about the sampling method (or lack thereof), especially the use of kids to establish age. I guess I can’t argue though with what Prudential wanted to show with the dotplot because they never talk about their intent. Average oldest person? Sure… it does seem gimmicky, right?

To be fair, one *should* be prepared to live longer than the average person now. First, it certainly is not unlikely to live longer than average. Second, given advancements in the next few decades, the average lifespan should be longer.

Regardless, I am sure there is a more appropriate question to ask for a good indicator of lifepan.

Dan · June 4, 2013 at 8:37 pm

Maybe this article reflects what’s called Muphry’s Law (sic). Broadly interpreted, someone reporting on an error is likely to make an error of the same category.

When planning for retirement, the objective is to avoid outliving one’s resources. It’s certainly reasonable to take into account a measure of the extreme case, to estimate the outer bound of probable outcomes. It would not be reasonable to determine retirement needs _solely_ on the basis of this curve, but the mean of the distribution, near 90, is not an outrageous starting point for guessing how long retirement assets may need to last. Of course, one should not make retirement plans on the basis of a single chart viewed in a TV commercial, especially this one.

But for the vast majority of people approaching retirement today, the number proffered in this article, 78, as the mean life expectancy (measured at birth), would be woefully inadequate, far worse as an initial guess than the low 90s. As others have mentioned, the average life expectancy of someone already at retirement age will be significantly higher than 78 years old. And _average_ life expectancy is for most people a very poor basis for estimating resources that will be needed in retirement. One must try to pick a low probability of outliving ones retirement resources, and the average age at death won’t give that. Some measure of the tail of the distribution should be looked at. “The oldest person you know” isn’t perfect, but it’s far better than the mean of the distribution.

MrHonner · June 4, 2013 at 9:44 pm

It wasn’t my intent to advocate for average life expectancy as the target for retirement planning, per se. As was mentioned by a previous commenter, the goal of retirement planning is to minimize the risk of outliving your resources, and something higher than the mean life expectancy would be the target age for most people.

But I don’t believe “average oldest known person” is a meaningful statistic here. The fact that it may be closer to someone’s target age is just coincidental.

Kate Owens (@katemath) · June 4, 2013 at 8:48 pm

Hey, that’s a really good point that I hadn’t thought of when I saw the Prudential commercial. I was too excited just to see a dot plot on TV! The points you raise make me wonder about several other related questions, like:

(a) Given that you have lived to age 65 and are the type of person to have been saving for your retirement for some number of years, what is your life expectancy? [Obviously, average life expectancy takes into account a lot of people who die much younger than retirement age, so somehow I’d be more interested in this conditional probability question.]

(b) How strong is the correlation between “average life expectancy” and “average age of oldest 1% of population”? I definitely agree that it isn’t clear that “average X” and “average highest known X” are not the same, but how closely does the increase in one track with the increase in the other? I mean, it seems possible that if the oldest person ever known by you is 10 years older than the oldest person ever known to your parents, this indicates that you will probably live longer than your parents — but by how much, and how confident can we be about this?

(c) What is the rate of change of the annual cost of living another year? Suppose I know I’m going to live to be 105 years old. Then what is the comparison of the cost of my 67th year to my 103rd year? I feel like I’d use more retirement money between 65 and 75 than I would between 95 and 105, but maybe this depends too heavily on the cost of medical care and my comparative health between these time periods.

MrHonner · June 4, 2013 at 9:56 pm

The conditional probability questions are interesting. Your comment reminded me of this NYT piece about the conditional life expectancies of New Yorkers. (http://cityroom.blogs.nytimes.com/2012/12/11/proof-of-citys-wholesomeness-new-yorkers-live-longer/). Presumably, people start saving long before they near retirement, and as those conditional life expectancies change, I suppose their retirement strategy would have to change as well. Sounds like an interesting Calculus problem!

Your second question is really interesting as well, however I think the fact that we “know” so many people somewhat obfuscates the relationship you are interested in. For example, millions of people know who Bob Barker is; for those millions of people, is 89 then the minimum possible age of the oldest person known?

Kate Owens (@katemath) · June 4, 2013 at 10:04 pm

Hmm, I inferred that “to know someone” in this context meant to know someone personally & probably someone with whom you share nontrivial genetic material, so I’d rule out Bob Barker. I wonder what the Prudential people meant by “to know”…

MrHonner · June 5, 2013 at 8:42 am

If we interpret “know” to mean “be related to”, then this data may in fact be meaningful. I would imagine life expectancy is genetically correlated to some degree.

Shashi Sathyanarayana · June 9, 2013 at 2:29 am

Misleading or not, the commercial is unique and offers much scope to introduce interesting topics in statistics and modeling. See http://www.numericinsight.blogspot.com